5 Interesting Learnings From Freshworks at ~$600,000,000 in ARR

"They’ve moved to half of their revenue from $50k+ deals, vs the $2k for smaller customers"

So we last checked in with Freshworks at $400m in ARR. Fast forward to today, and last quarter they crossed an incredible $560,000,000 in ARR growing 20% on a constant currency basis. That should put them at about $600m ARR today!

5 Interesting Learnings:

#1. Bigger Customers Keep Growing, But SMBs Have Slowed

A common theme across tech today. Freshworks has 51,700 customers at around $2k ARR, with a quick close of just 25 days. But in contrast to their bigger customers, the macro environment — or perhaps market saturation — has led to slowing growth in this segment in 2023.

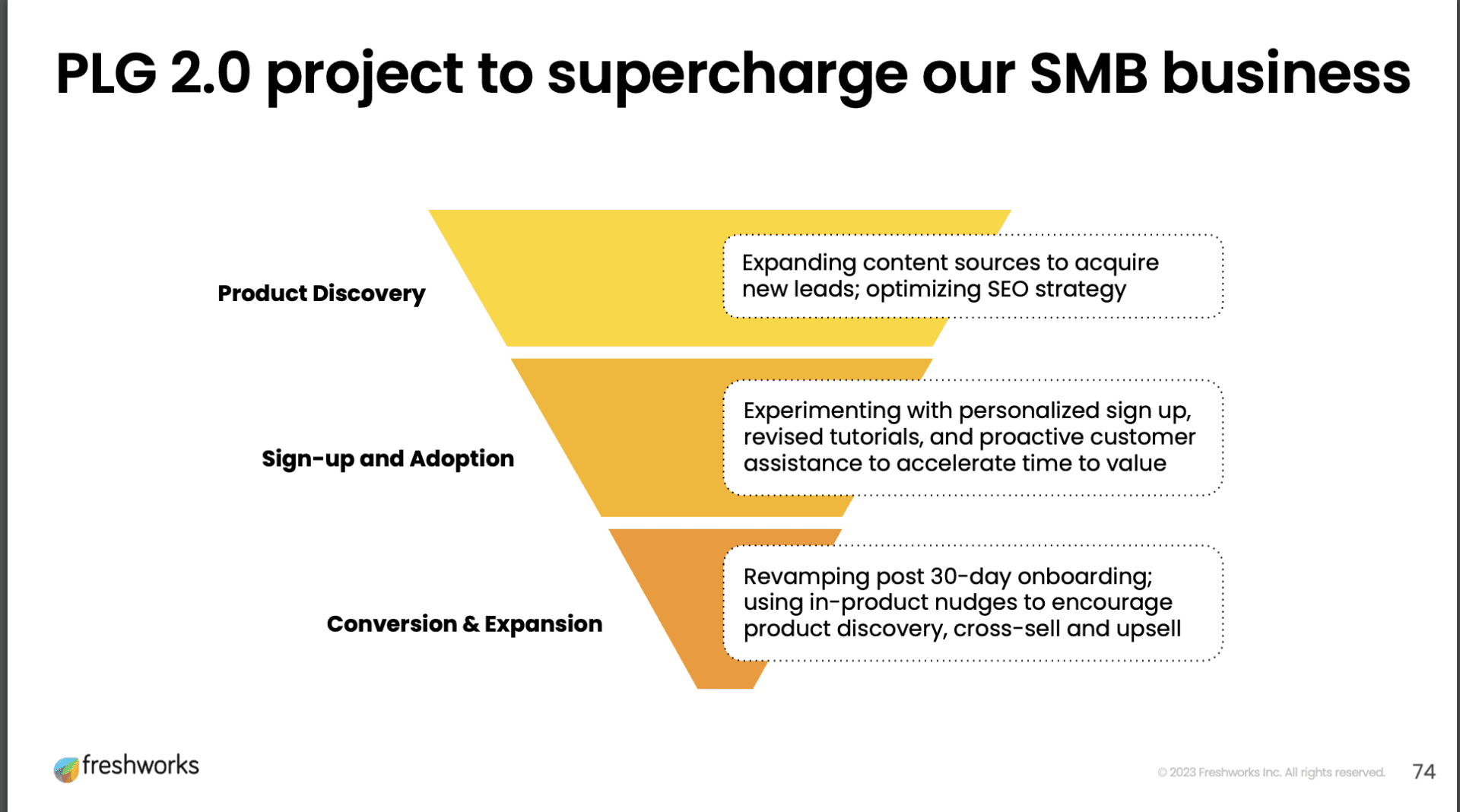

#2. Leveling Up PLG to Accelerate SMB Customers, Including More Attention to Onboarding

I love seeing this, it can seem hard to invest heavily in small customers, but if you don’t especially invest in onboarding, that’s a big shame. Because there are few things worse than closing a customer that never actually uses your product. So much wasted energy getting them there.

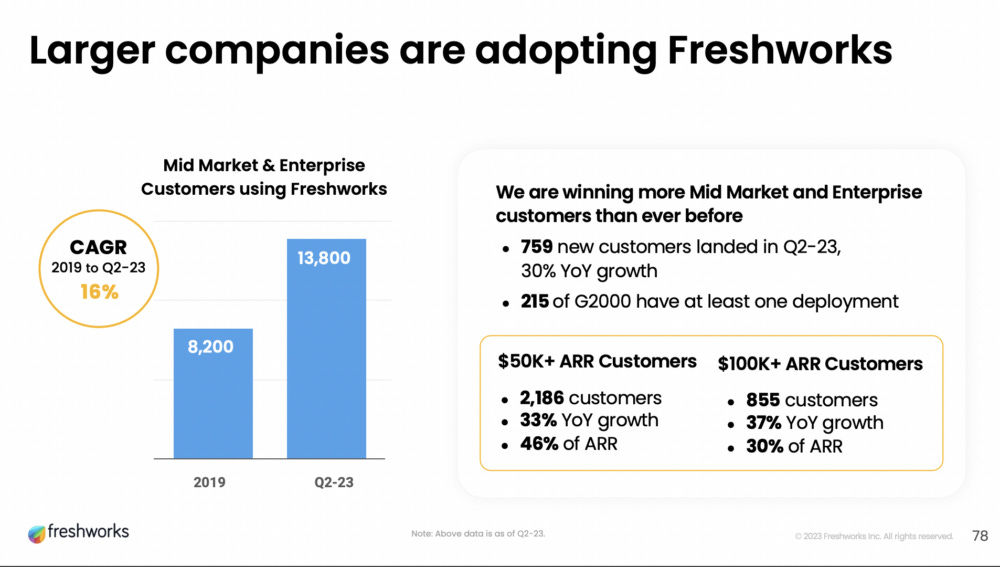

#3. The Big Growth Today is In $50k+ and $100k+ Customers. Soon, They Will Be The Majority of Revenue.

Not a surprise per se, other somewhat similar players are seeing the same thing. But good to learn from. $50k customers are growing 33% (vs 20% overall) and $100k+ customers are growing 37%. Soon, the majority of Freshworks’ revenue will be $50k+ customers. A big change from their roots with smaller SMBs.

#4. Automation / AI is Already a Big Deal. Over 220,000,000 Transactions Are Automated in Whole or Part.

The contact and support spaces have rapidly adopted as much of AI as they can. Automating tickets and support is a huge industry theme, and Freshworks has already automated 220,000,000 interactions, in whole or part.

#5. Moved to 71% Annual Contracts (From 54% in 2019) As Have Gone More Enterprise

This is what I’d expect, but very helpful to see this data presented this way, as they’ve moved to half of their revenue from $50k+ deals, vs the $2k for smaller customers:

And a few bonus learnings:

#6. NRR Stable / Up a Smidge at 108%, But Boosted By Price Increases

Like Monday and many other leaders that sell to SMBs, they’ve seen some decline in NRR. It remains relatively strong at 108%, however. But a 3% price boost likely materially helped.

#7. Like Almost Every Other SaaS Leader, Freshworks Has Gotten Much, Much More Efficient. Free Cash Flow Has Swung From -3% to +10% in One Year.

Like just about every other Cloud leader, Freshworks has gotten much, much more efficient in the past 12-18 months. In 2022, they had negative free cash flow of -3%. Just a year later, they are at +10%. That’s radically more efficient.

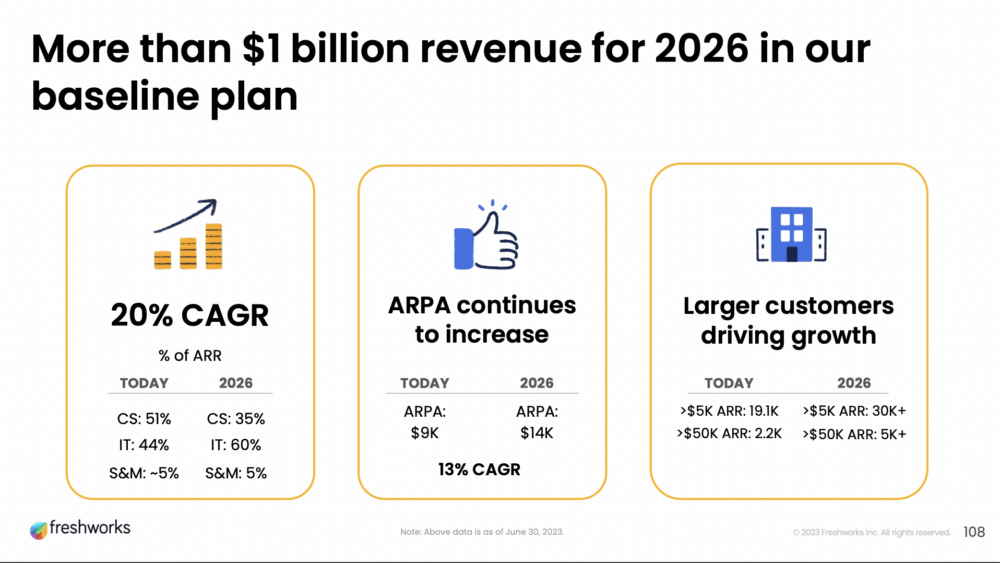

#8. Predicting $1 Billion in ARR in 2026

The power of > 100% NRR. You can pretty reliably predict revenue over the coming years. Freshworks clearly sees $1B in ARR bu 2026. That’s just math, really. And a ton of really hard work 🙂

Wow what a run! See you at $1 Billion in ARR, Freshworks!

“This edition of the SaaStr is sponsored by SAP:

Learn how the pre-integrated public cloud ERP from SAP can uniquely support the requirements for Everything as a Service (XaaS) for both product-centric and service-centric organizations. Register here.”