Unicorn Production in Down 80%. And Falling.

And Why Some Startup Financial Models Can Lead to Ruin

So Openview has a bunch of great metrics in its latest SaaS Benchmark report here.

One that stood out to me was this great chart summarizing the steep fall in Unicorn production (which in turn is sourced from CB Insights);

Unicorn “production” has now fallen 80%-85% in Q3, and probably has further to fall. At the peak of 2021, 40 Unicorns were being minted every month. It really was like that. Now we’re down to 8 — and falling.

Yes, you might be one of the 8. I hope you are. Just share the chart above with any of your cofounders or teammates who don’t quite have a sense of how things have shifted lately.

Having said all that, there are 2 different ways I see this chart:

On the one hand, unicorn production has fallen 80%-85%. Ouch!

On the other hand, it seems to just sort of be back … to “normal”. To where it was before the Covid Boom in SaaS and Cloud. We’re back to roughly minting as many unicorns as we did back then, when SaaS was … hard.

So the real danger I see, as do other SaaS veterans, is with folks who weren’t founders and execs before the Boom. They don’t remember what SaaS used to be like. That it was hard. That sales and marketing and success had to be a lot more efficient than they have been. That sales teams have to close 4x or more what they take home, not 2x.

And this infographic may not be fun, but it does a good job of explaining venture today:

Ops Folks Build Smart Financial Models. But They Are Often Dangerous.

So I’ve seen a trend among many startups these days which is to sort of have a VP or Director of Business Ops instead of a VP / Director of Finance. They handle the cash too, but also go deep on the business in a way a “finance person” usually simply can’t.

These folks often come from strategy consulting or banking backgrounds. And they are often great hires, often very smart.

But here’s the thing: they build GIGO financial plans. Garbage In, Garbage Out.

What do I mean? The smart folks at Bain, at McKinsey, at Morgan Stanley, etc. will build a financial plan to tell you what you want to hear. E.g.:

If our CAC just goes down, we can stretch the cash 2 years.

If our sales efficiency just goes up, our cash lasts 30 months.

And most dangerously, if growth accelerates just a bit, then … well … we hit the plan!

This type of modeling is what you do when you are selling. You sell various scenarios, and the ex-consultants and ex-bankers and ex-VC analysts are great at it. They tweak things, the inputs and variables, to achieve the desired outcome.

True finance folks (e.g., Controllers, CFOs, VP of Finance) usually don’t do this. In fact, they usually don’t know how. Instead, they tend to build financial and operating models that are very much driven in the present. In today’s burn, and today’s revenue, and today’s issues.

That can be frustrating, when you want to model a stretch plan and a super stretch plan. Most controllers, in my experience, can’t do it. They aren’t great at helping you build a C-10 plan. But they can give you a very honest answer to how long your cash lasts.

The fancy GIGO model, by contrast, can make everything look roses next year. And when it doesn’t happen IRL, the money runs out far faster than anyone planned.

I’ve seen this so many times, again and again. The “model” for this year and next year having its inputs manipulated by a very smart ex-banker/consultant/VC analyst to produce a desired outcome.

Be wary.

At least, don’t run your business and especially now your Zero Cash Date on these models.

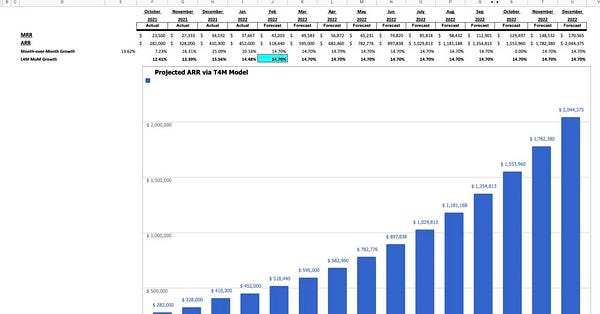

And no matter what, force your VP of Ops to also build an L4M Model. A model just based on the last 4 months of real results. Here’s how to do just that. In just 15 minutes, in fact: