The State of SaaS Go-to-Market with Theory Ventures General Partner Tomasz Tunguz

This edition is sponsored in part by Adyen: How leading SaaS platforms have adopted embedded payments

When Marc Benioff started Salesforce, he codified the sales playbook. Then Mark Roberge, former Hubspot CRO, wrote The Sales Acceleration Formula with deep insights into quota structures. For the subsequent ten years in software, we’ve optimized every little bit of how we sell it.

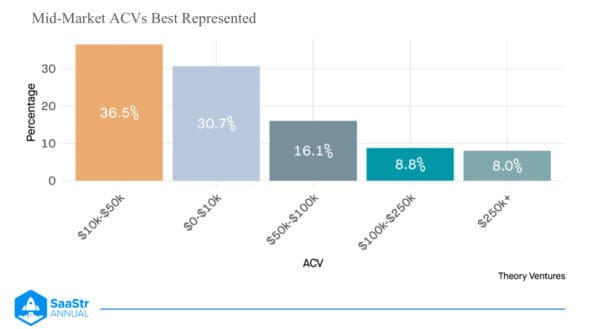

But today, it’s different because the kinds of software we sell aren’t the same. It isn’t predictable. Six months ago, security was the number one prohibition preventing businesses and software companies from buying AI. Today it’s ROI. Tomasz Tunguz, General Partner at Theory Ventures, shares nine observations from a Go-To-Market survey Theory Ventures did with hundreds of startups, 68% of them early-stage, well-funded, mostly mid-market ACV, and 25% remote. Here’s what they found.

#1: Founders Are More Positive

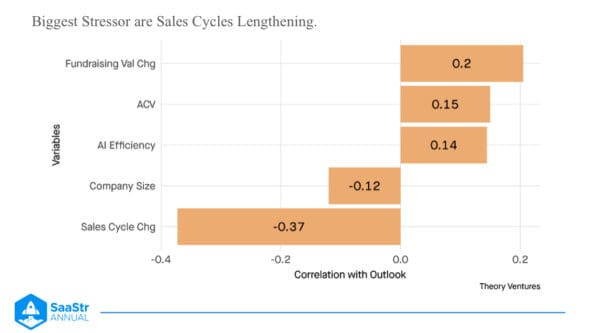

The average founder’s outlook increased from 6.1 at the height of 2022 to 6.7. That’s a statistically significant increase in the overall positivity of founders. The biggest challenge to that outlook is an increase in the sales cycle.

In 2020, we transitioned from a physical selling universe to a virtual selling universe. That elongated sales cycle created pipeline supply shocks. If your sales cycle doubles, you’re bookings are cut in half with a massive lack of predictability. This can destabilize your business and have a big impact on cash.

It’s no surprise that sales cycle length is the biggest driver of optimism or negativity in the ecosystem. This creates a much harder capital markets environment. US venture funding went from 8 to 300 over 15 years. It’s now falling to 150 because 81% percent of the dollars invested in venture capital at the height of the boom came from non-traditional venture capital firms which are all very likely to leave investing.

But what we see within the founder universe is people are pretty positive. In the fundraising ecosystem, even as the public market multiples have collapsed we’ve seen Snowflake go from about 25 to trading at an 8 times forward multiple in the last 18 months. So private markets have been resolute and resolved to keep their positivity.

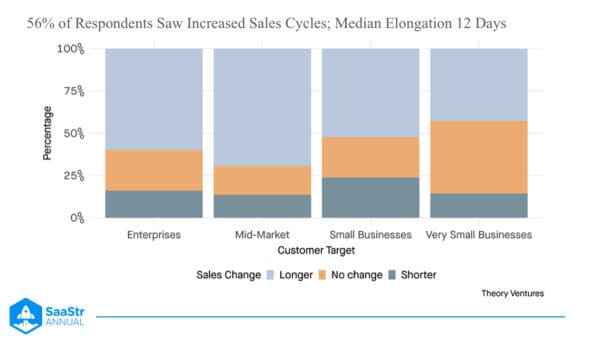

#2: Sales Cycles Are Longer

Half of all respondents saw an increase in their sales cycle, most notably in the mid-market. Why is the mid-market harder? Theory’s rationale is that the CFO is tightening its purse strings and eliminating discretionary budget at the mid-manager level.

So, if an executive wants Enterprise software, they can bypass procurement. On the flip side, if an individual wants to try something and they’re at the bottom of the market for $20/ month, they pull out a credit card and sign up. Bottom-up PLG and very top-down are relatively healthy. But mid-market is the hardest place to be across all software right now.

If you imagine, you have essentially 40% over-provisioning of seats. Tomasz shared an example of a friend of his who was part of a cost-cutting exercise at a major publicly traded company. They had signed a three-year, 100 million infrastructure deal and ultimately saw a less than 3 percent utilization.

Where did that come from?

It likely came from a mid-manager. And so as a result, that lengthens sales cycles within mid-market. That’s where things are the most challenging. And this is true across all of software and AI.

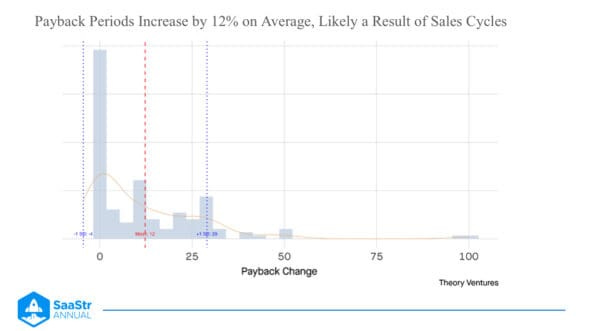

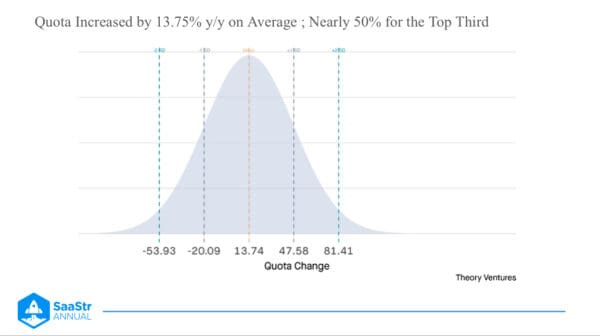

#3: Payback Periods + Quotas Have Jointly Increased

The number of months required to recoup the cost of customer acquisition has increased by 12% on average, which is linear with the increase in sales cycles. To offset slower sales cycles and worse payback periods, quotas have moved in step with them.

The average respondent increased their quota by 14% year over year, which is higher than inflation, which is around 4% per year. We’re looking at more than double the inflation in sales quotas.

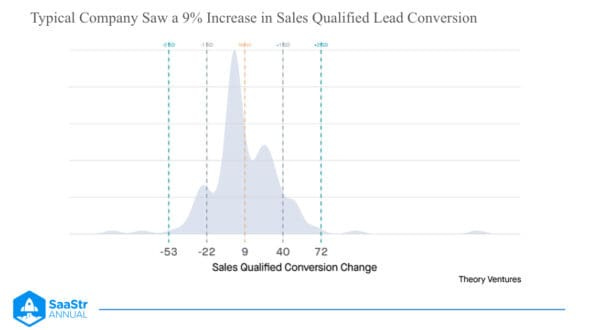

#4: Increased Scrutiny From Software Buyers

Even though founders remain more optimistic than ever, buyer scrutiny has increased, and what they buy has a higher qualification rate. The GTM survey shows a 10% increase in sales-qualified conversions and a 40% increase in sales-qualified conversions for the top third of these businesses.

Why? Theory hypothesized that if you have a large pipeline as a sales leader and you’re not hitting your numbers, you’ll likely redefine your ICP and qualification criteria to narrow down the funnel and focus on your core buyer a lot more. So while It may take longer to sell to them, they’re more likely to buy.

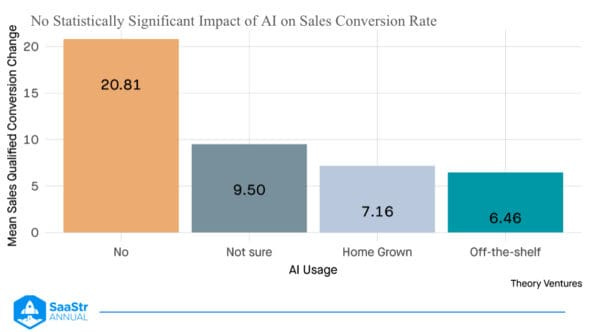

#5: AI Isn’t Impacting Conversion Rate

Companies can now deploy a sales copilot or utilize full SDR automation fairly quickly. So the survey asked how much as a business has AI impacted its sales funnel.

There was actually no difference in performance when looking at bookings of a company or their lead conversion rate regardless of whether or not they used AI. So it doesn’t matter today. There’s no change in the ultimate conversion rate as a function of using AI or not.

Tomasz was chatting with the CRO of a publicly traded company, and asked her if she was using an AI SDR. She said yes, so he asked how it’s going.

And she said ‘you would not believe the amount of pipeline we’ve been able to generate with an AI SDR. ‘

Great! So how much business has it closed?

Zero.

So it’s not to say that AI won’t work. It’s to say many of us do not know how to use AI effectively enough yet to impact conversion metrics.

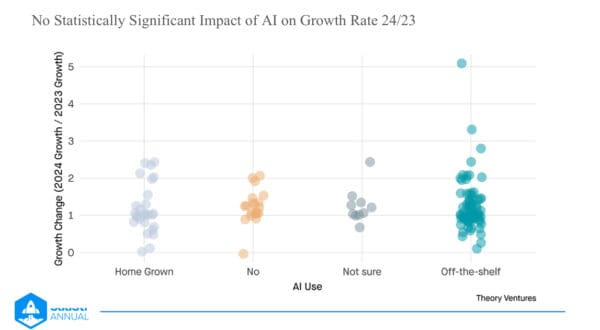

#6: AI Has No Noticeable Impact on ARR Growth

Next question the survey asked of startups was, ‘if you use AI, is your growth rate meaningfully faster than you thought it would be year-over-year?’ The answer was no. This survey shows no noticeable impact on overall growth rate change as a function of using AI, all the respondents were effectively identical.

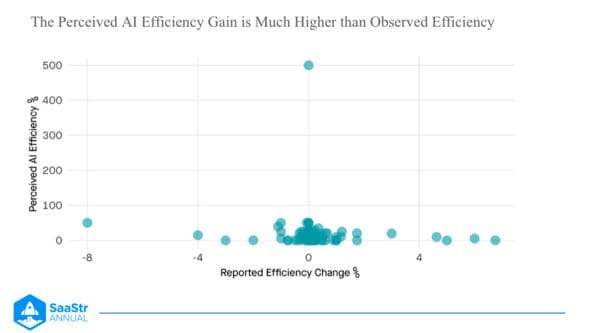

#7: AI Efficiency Gain: Perceived vs. Measurable

How much did these companies grow, and how efficient was that growth thanks to AI? One outlier said they were 5x more efficient with AI while the majority responded that they were somewhere between 25%-75% more efficient. However, when Theory layered in the actual data to see how much more efficient they were year-over-year, the numbers were between -4% and 4%.

There is a dominant belief that AI makes processes more efficient, but this belief has not yet been confirmed by the data.

#8: 3x Net Dollar Retention Thanks to This Pricing Model

Over time, the dominant pricing structure in B2C and B2B applications is like the cell phone plan. You get a base number of minutes for a particular price. You might buy 500 extra minutes at a cent per minute. You pay an additional 2.5 cents per minute if you want more than that. That’s called a 3-part tariff.

Many SaaS companies have copied this for a long time as a two-part tariff: a base platform fee upfront then the incremental cost of additional users as you go. But now there’s been a broad shift toward usage-based pricing or seat-based pricing, or a combination of the two.

If you look at the net dollar retention change, the top quartile used to be 130% pre-2020. Now, it’s about 120%. If you look at NDR with the combination pricing model of seats plus usage, you see 3x growth compared to any other form of pricing.

The idea with a three-part tariff is that you’re able to charge for value. You generate 10 million worth of marginal ROI, and you’re able to capture 15, maybe 20, maybe 25 percent of it. So the combination pricing strategy of a base platform fee plus a usage-based component plus value is what’s driving the market today.

Key Takeaways From Theory Ventures GTM Survey

We’ve noticed founders are more positive despite sales cycles being 12% longer

The lengthening sales cycle increases the payback period to offset it

Startup founders and CEOs have increased their sales team quotas linearly

AI today has no impact on conversion rate

AI does not impact ARR growth, even though people who buy AI perceive it as meaningfully contributing to overall efficiency gains

If you’re considering changing your pricing model, consider creating a hybrid or matrix pricing model. You’ll have six percentage points more of net dollar retention, and as Einstein said, compound interest is the most valuable force in the world.

This edition is sponsored in part by Adyen

How leading SaaS platforms have adopted embedded payments

CFOs from SaaS platforms in the insurance and legal industries reveal how embedded payments are transforming their revenue streams