5 Interesting Learnings from Zscaler at $2.5 Billion in ARR

"Growth isn’t quite as crazy as it was at $1.5B ARR (46%). But — there’s no downturn at Zscaler. None at all."

So Zscaler is a security juggernaut well known to everyone in the industry, but for whatever reasons, it doesn’t quite get as much attention outside of it. Wiz’s epic growth — and saying No to Google’s $22B offer — gets the attention. More obscure (but still important) vendors like Darktrace get attention due to their founder. CrowdStrike got even more attention due to a bit of a patch mishap.

But for folks outside of cybersecurity, Zscaler doesn’t quite get the attention it should.

Because it’s epic:

$2.5 Billion in ARR

Growing a stunning 30% still (!)

27%+ free-cash flow margins

a $26 Billion market cap (!) or 10x ARR

a wildly successful and committed repeat founder CEO who did it again, just much bigger

Growth isn’t quite as crazy as it was at $1.5B ARR (46%). But — there’s no downturn at Zscaler. None at all.

5 Interesting Learnings:

#1. A Record Quarter with $911 Million in Bookings!

Zscaler’s growth has slowed somewhat from the even more epic rates at $1B and $1.5B ARR, but it’s still setting records. Billings in Q44’24 were a record $911,000,000! Or maybe even $1B (both numbers are cited). Either way, huge.

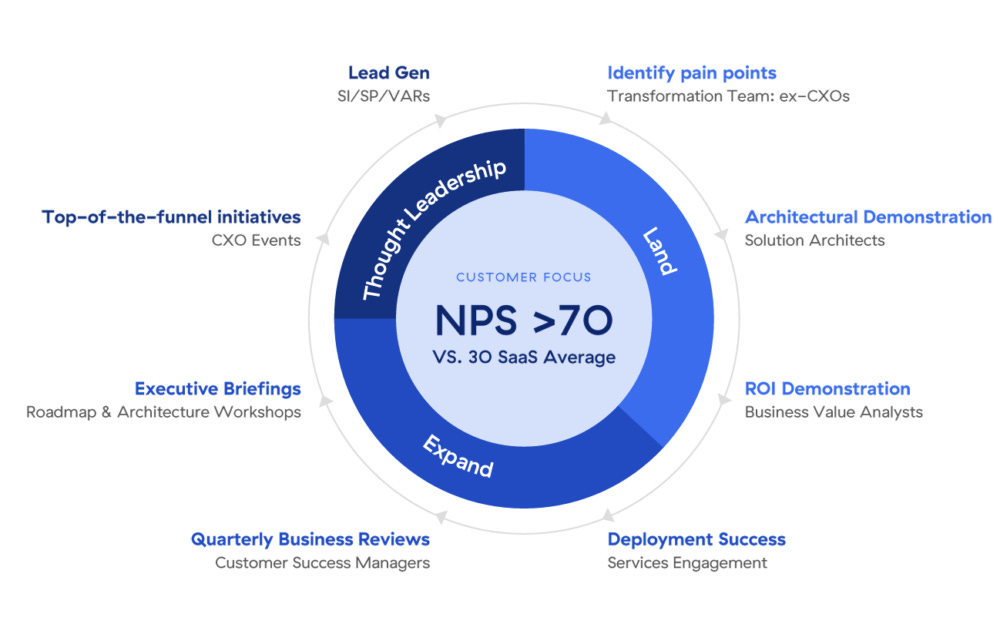

#2. 70 NPS, Even at $2.5 Billion in ARR

Is NPS a slightly subjective metric? Sure. But getting a 70 is still truly world class. And perhaps what it takes to go so long in such a competitive space.

#3. 3,100 $100k+ Customers, Up From 973 in 2020. And 567 $1m+ Customers.

Zscaler has customers Small, Medium and Large, but overall its approach is pretty enterprise. 35% of the Global 2000 are customers, and it has over 3,000 $100k+ customers and 567 $1M+ ARR customers.

#4. 115% NRR. Down From 125%, But Still World Class

115% NRR, 30% revenue growth, and a 34% CAGR in $100k+ customers suggest a strong next 5+ years for Zscaler. NRR though is still down from 125% at $1.5B ARR.

#5. Not Hyper Efficient … But Still Very Efficient, and Much More So Than Before

Zscaler is generating a ton of cash, but on a non-GAAP basis isn’t quite profitable due to equity expense (SBC). Still, it’s still very efficient, and far more so than 2020-2022. This is what the markets want. Not just profitability per se. But strong, strong growth paired with a reasonably efficient model. That’s Zscaler. It’s gotten more efficient. But it’s still investing in the future. Not harvesting the present and the past.

And a few other interesting learnings:

#6. New / Emerging Products Now Mid 20% of New Business

A reminder we all need to continue to drive to be truly multi-product.

#7. Typically Sign 3 Year Contracts, First Year Paid Upfront

This isn’t uncommon in the enterprise, but it’s a very classical approach to software contracts. It works for Zscaler.

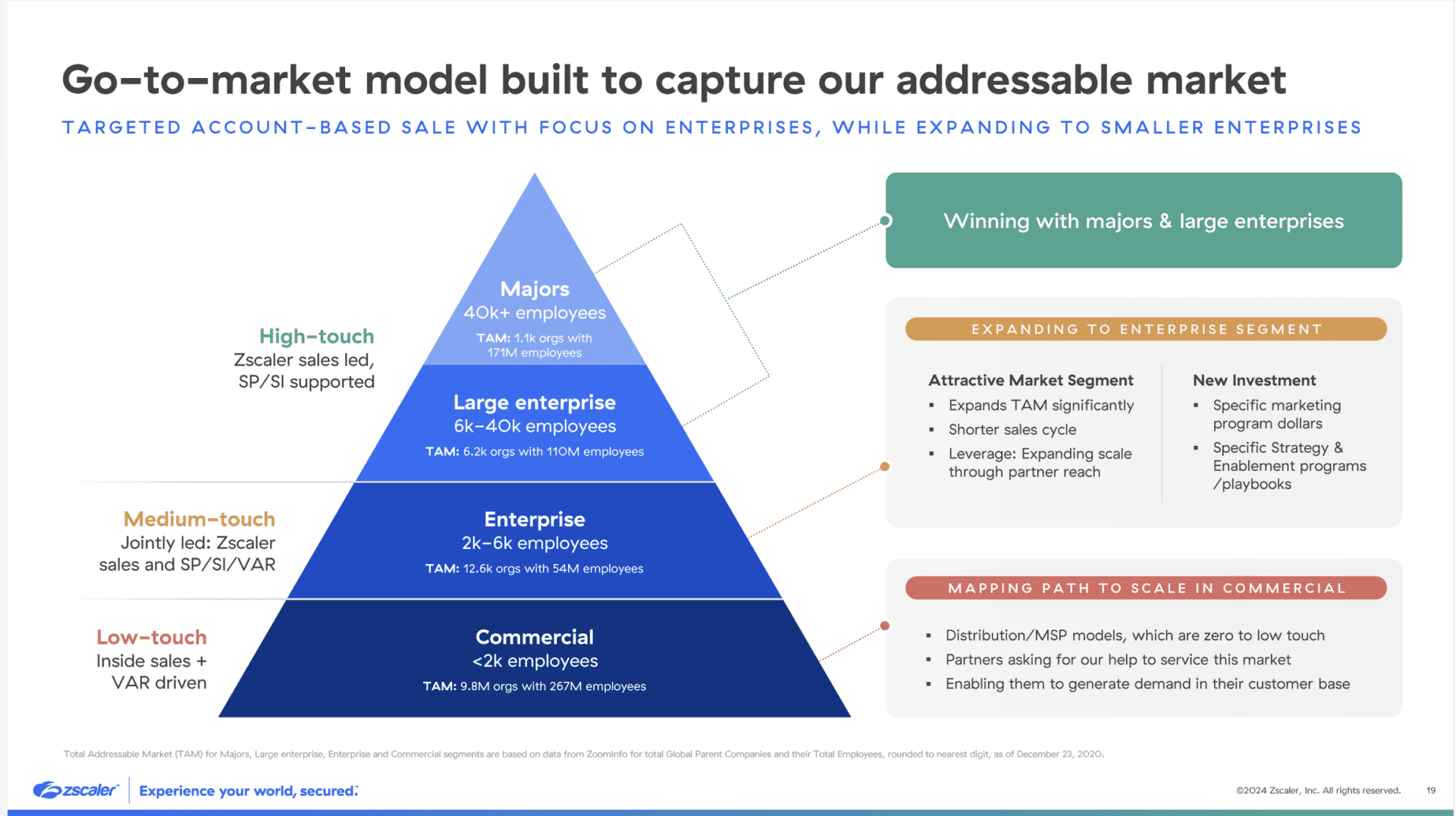

#8. Vast Majority of Revenue Comes in Part or in Whole from the Channel.

Back in 2021, 94% of Zscaler’s revenue came in part or in whole from channel partners, from SIs at the high end to VARs at the low end. They don’t disclose the exact percentage today, but it’s likely close to that today as well. So many enterprise sales are really through the channel — and not direct sales. A reminder to not be too reliant on direct sales alone, as so many startups are.

#9. Overall Demand is Stronger Than Ever, and New Logos Have Doubled

Zscaler is clear: there’s no downturn. Not for them, at least. And new logos are being added at a record rate, doubling according to CEO Jay Chaudhry. Is there still higher scrutiny on spend? Yes. But it’s something you have to push through. Zscaler also feels it benefits from that environment because “We’re in a unique position to remove a number of point products that help justify closing our deals.”

Go Zscaler, Go!

Is Zscaler in a competitive market? Yes

Is spending still under scrutiny overall? Yes

Has it had to continually innovate to stay ahead? Yes

Is it facing some “law of large number” issues at $2.5B ARR? Maybe

But it’s still going at epic rates. Growing 30% at $2.5B in ARR. Let that be a challenge to all of us!