5 Interesting Learnings From Workday at $9 Billion in ARR

"30% of All Customer Expansions Involved AI Products. And It’s Already Leading to ACV Expansion."

So who will benefit the most from AI in B2B? The hot new start-ups, rocketing to $100m ARR in record time? Or … the established leaders, who can add AI onto their apps and not just expose vastly more functionality, but leverage all that existing customer data, to create something brand new and fresh?

We’re watching. AI has already completely rebooted many older leaders in the contact center, from Zendesk to Genesys to Intercom, which now are truly AI-first and thus in many ways radically different than they were just a few years ago. And ServiceNow seems to be on that journey. Salesforce is on it, too.

And what about Workday? The grandad of HR SaaS, Workday? How is The of AI changing it? Well, it’s early. But Workday remains a force of nature:

Almost $9 Billion in ARR

Growing 15%, so adding well over $1B in new bookings a year!

Subscription backlog up 19.7%, to $25 Billion (!). So a huge amount of revenue booked but still to come.

27%+ Free Cash Flow margins, 26% non-GAAP profit margins, and $8 Billion in the bank, so generating massive cash

$57 Billion market cap, so trading at 6x+ ARR

Workday is 20 years old this year. And in many ways, it’s just getting going. Pretty impressive.

5 Interesting Learnings:

#1. 98% GRR. No One Leaves Workday. No One.

There’s enterprise software … and then there are folks like Workday and ServiceNow with 98%+ GRR. Where literally, on one leaves. Now when I was a VP at Adobe, I saw them deploy it and I get it. It tooks years to roll our Workday there, but when they finally did, it literally was embedded in every facet of how the company was run internally. Moving off would likely take half a decade.

#2. Very Focused on AI Agents as The Future

Workday is trying to leverage AI to remain the core system of record in HR and financials in the enterprise. And they want Workday to manage all your agents.

#3. 11,000 Customers, So $820,000 ACV on Average Per Customer

That’s pretty enterprise. Workday is a $1m+ a year and up solution for the Big Guys.

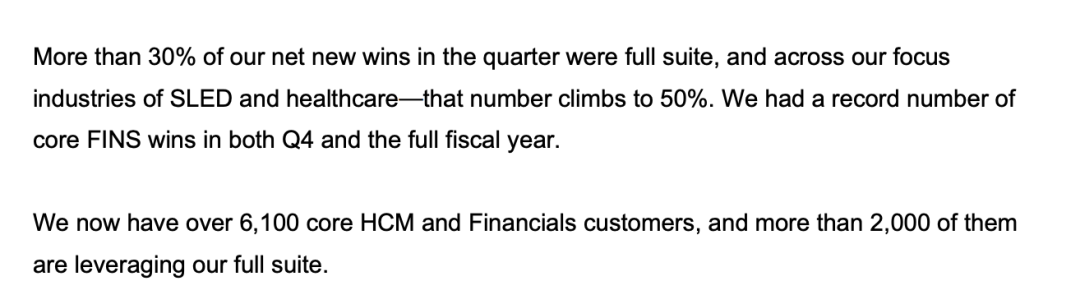

#4. 30% of New Customers Are “Multi-Suite”, Buying Both CRM and Financials and More

Yes, Workday is huge. But a reminder of how critical being multi-product is to scaling.

#5. 30% of All Customer Expansions Involved AI Products. And It’s Already Leading to ACV Expansion.

That’s AI in the enterprise today. Is it all magic today? Not always. But it’s where the incremental budget is in the enterprise.

And a few other interesting learnings:

#6. 20,400 Employees, So About $440,000 in Revenue Per Employee

Not bad but merely “very efficient”. In any event, $400,000+ is where most B2B leaders are aiming for by IPO at least. They also reduced the workforce by 8% despite the strong growth to get even more efficient.

#7. Professional Services is $700 Million, or About 8% of Revenue

Workday like Salesforce needs to do a ton of services to get deployments going, but they mostly outsource is to third parties. But they still need to do it, so when it’s important, they do some of it in-house. The real number of dollars going into Workday deployments per year is many billions, but most is done by partners.

Wow, what an engine at Workday. Growing 15% at $9 Billion, but with a backlog growing almost 20%. And AI is driving up deal sizes, with high attach rates.

Don’t bet against the leaders in B2B and SaaS falling behind due to AI. They’re all over it. And we just don’t know yet who wins the most.