5 Interesting Learnings from Toast at $1.5 Billion in ARR

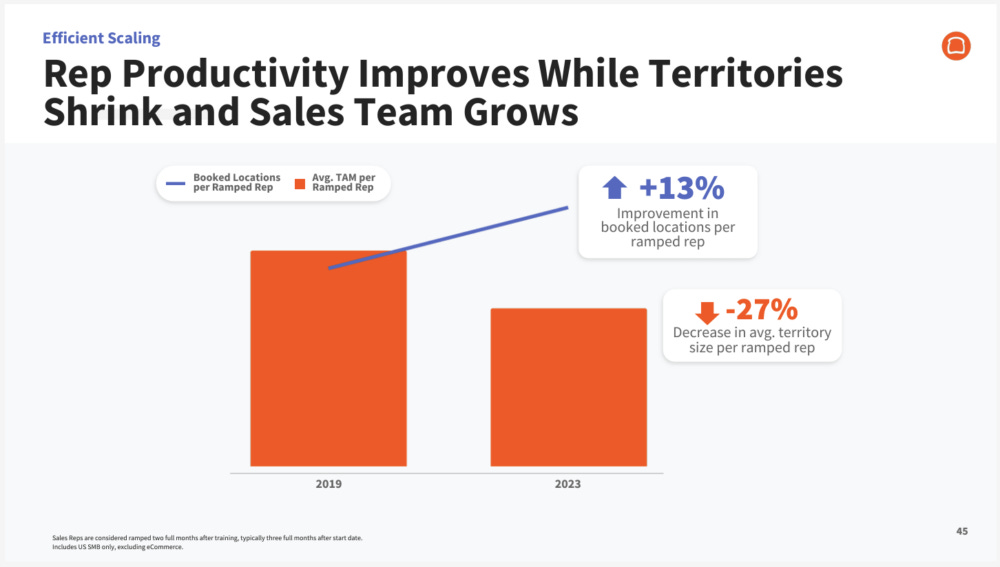

"A lot of sales reps won’t like to see this, but Toast got more efficient by forcing its sales reps to be more productive from smaller territories."

So times are tougher these days for many, but in B2B2C … less so. Shopify is seeing growth accelerate. Canva is on fire at $2.4 Billion+ ARR, growing 40%, on the way to an IPO. And Toast is similarly executing at a high level. No downturn there.

It’s at $1.3 Billion in ARR, growing a stunning 29%. Boom! And importantly, like Shopify, they expect that level of growth to continue.

And for that, they’ve earned a $13.5 Billion valuation. This is what one 10x ARR leader really looks like.

5 Interesting Learnings:

#1. Grew Restaurant Locations 29% Year-Over-Year to 120,000

Perhaps the most important metric at scale. Are you growing net new customers at least 20% a year? HubSpot is, and Toast is as well.

#2. Only 18% of Revenue From SaaS. 80% from Transaction Fees.

Shopify and Bill both also get the majority of their revenue from financial fees and transaction fees, not software subscriptions. But Toast even more so, at 18% of revenue. It’s probably not really a SaaS company, but close enough to include it in our series and our ecosystem.

#3. But Gross Margins Only 28% on Payments and Related Solutions

Low gross margins on payments and financial services of only 28% makes Toast’s model much tougher than Shopify’s (39% gross margins on payments) or Bill’s (80%+). They are now profitable, but it’s not easy when 80% of your revenue only has 20%-28% gross margins.

#4. Only Grew Sales & Marketing Expense 12%, and Cut R&D (Product + Engineering) and G&A Expenses

Toast has gotten to profitability by truly holding the line on headcount and revenue expenses. Sales & Marketing has only grown 12% as revenue has grown 29%, and R&D expense actually went … down.

#5. Crossed Over into GAAP Profitable, With Strong EBITDA

It was hard work, took some layoffs and effectively close to a hiring freeze, but it worked. Toast is now GAAP net income positive and adjusted EBITDA is strong, at almost a $400m run-rate. Toast is projecting adjusting EBITDA going forward of $300m+ a year, again strong numbers, especially given their low gross margins.

And a few other interesting learnings:

#6. Shrinking Territories, Increased Quotas Lead to Improvements in Sales & Marketing Costs

A lot of sales reps won’t like to see this, but Toast got more efficient by forcing its sales reps to be more productive from smaller territories. Reps hate this, but it does seem to have worked, at least for now.

#7. 13% Market Share in U.S. By Their Calculations

It does seem like Toast is everywhere, and the dominant vendor in restaurants. But the reality is overall the market is more fragmented than it looks, and Toast sees itself as having about 13% market share. And they’ve just begun to go international.

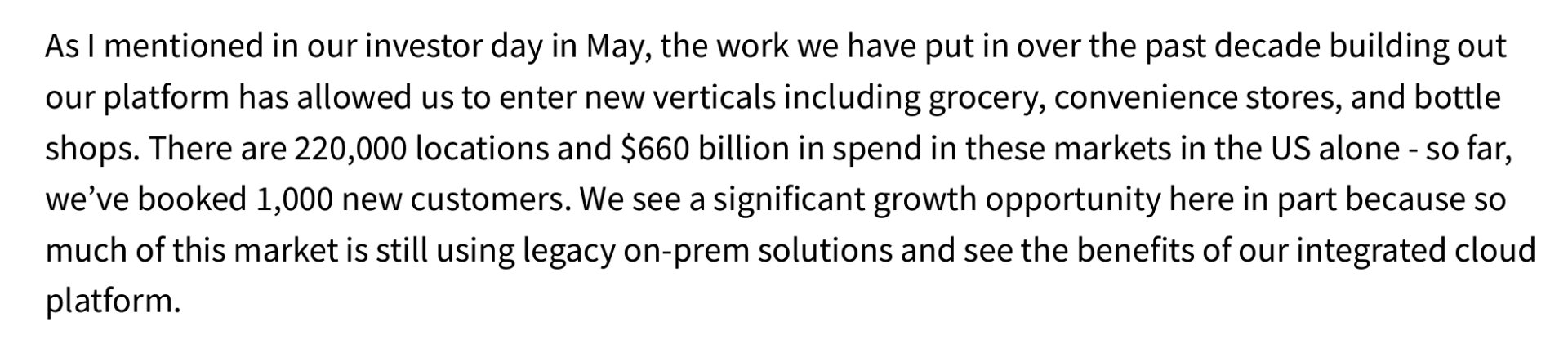

#8. TAM Expansion Coming from Grocery Stores, Convenience Stores and Bottle Shops

The restaurant industry is huge, and Toast has been able to get to $1.5 Billion in ARR serving mainly one industry in the U.S. (albeit a massive one). Restaurants have $1 Trillion in sales and are about 4% of the U.S. economy. But it’s now pushing deeper both into international and into other verticals to sustain growth.

#9. Customer Referrals Now Responsible for 14% of New Locations

Invest in true customer happiness, folks.

#10. Predicting 29% Growth Going Forward, Too.

Perhaps the most impressive of all. Toast is predicting this growth rates continues, while many SaaS leaders are seeing growth decelerate these days, or stay low.