5 Interesting Learnings from Snowflake at ~$4 Billion in ARR

"It’s Good Times Again, Just Different Good Times. Fueled by AI, not post-pandemic spend. And Snowflake is back on a tear."

So Snowflake looked immortal in 2021, looked a little more mortal in 2024 … and is now, like many of the best in Cloud and B2B, re-acclerating in 2025!

And come meet and hear from CEO Sridhar Ramaswamy LIVE at 2025 SaaStr Annual, May 13-15 in SF Bay!!

Snowflake is on a tear again:

$4B ARR (just about)

28% revenue growth

44% free-cash flow last quarter (WOW!), 26% for the year

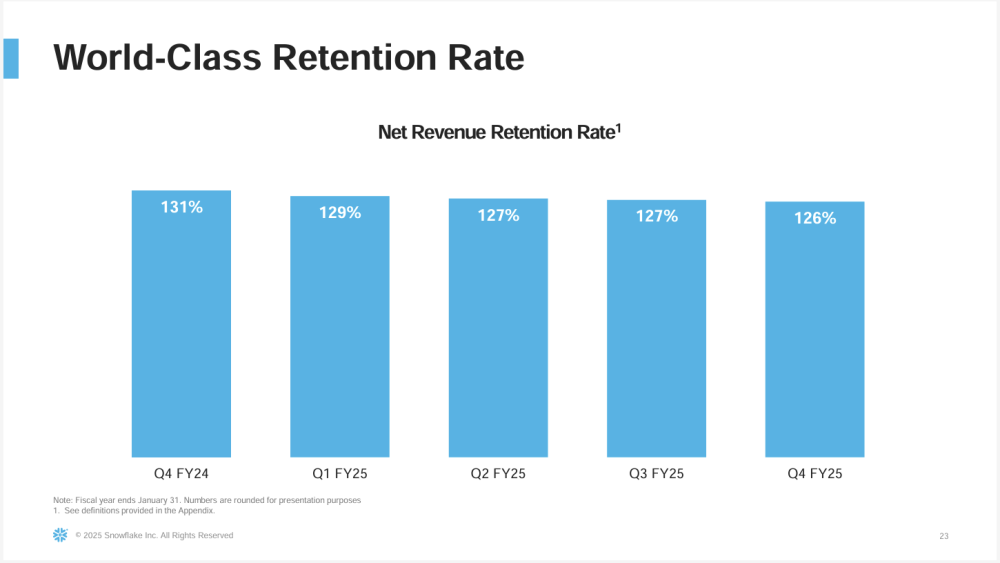

126% NRR

It’s not 2021. No, it’s 2025. It’s Good Times Again, Just Different Good Times. Fueled by AI, not post-pandemic spend.

And Snowflake is back on a tear.

5 Interesting Learnings:

#1. 11,159 Customers — So An Average of $360,000 Per Customer

Snowflake solves enterprise-grade problems around data management — and it charges prices commensurate with that. 580 of them pay $1m or more.

#2. 126% NRR and Staying High

While down a smidge from 131% in 5 quarters ago, this is still world class. And it promises a strong run of growth for Snowflake in the coming years. Snowflake is also predicting it will stay in the “mid-twenties.”

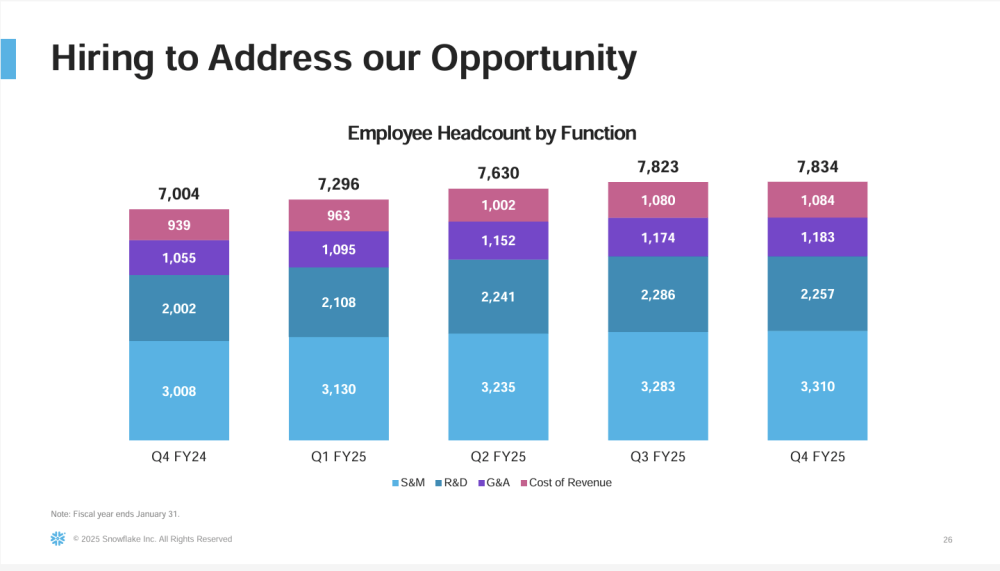

#3. Very Profitable Now, But Still Hiring

Snowflake has become a cash-generating engine, with 26% free cash flow for the past year and a stunning 44% (!) last quarter. But it’s still hiring, albeit more slowly that revenue. Hiring is up +12% over the past 15 months, and +8% over the past year. Revenue grew 28%, so that makes the company much more efficient. Even while it still hires. Hire, but slower than revenue grows, you get more efficient 😉

#4. 79% of Revenue Still From Americas

While different data and privacy laws and regulatory frameworks can make flowing data across borders harder than applications, I’m still a bit surprised Snowflake hasn’t increased its EMEA and APJ revenue. It can be hard. Will be interesting to continue to track here.

#5. 4,000 Customers Using Their AL and ML Offerings Weekly, But Direct Incremental Revenue Here Not Yet Material

It’s still early, but over 30% using their AI/ML offerings is a promising start!

And a few other interesting learnings:

#6. Customers Typically Sign a 3 Year Contract, Billed Annually Upfront

Not a total surprise in $1M+ deals, and takes some of the variability out of pricing as well.

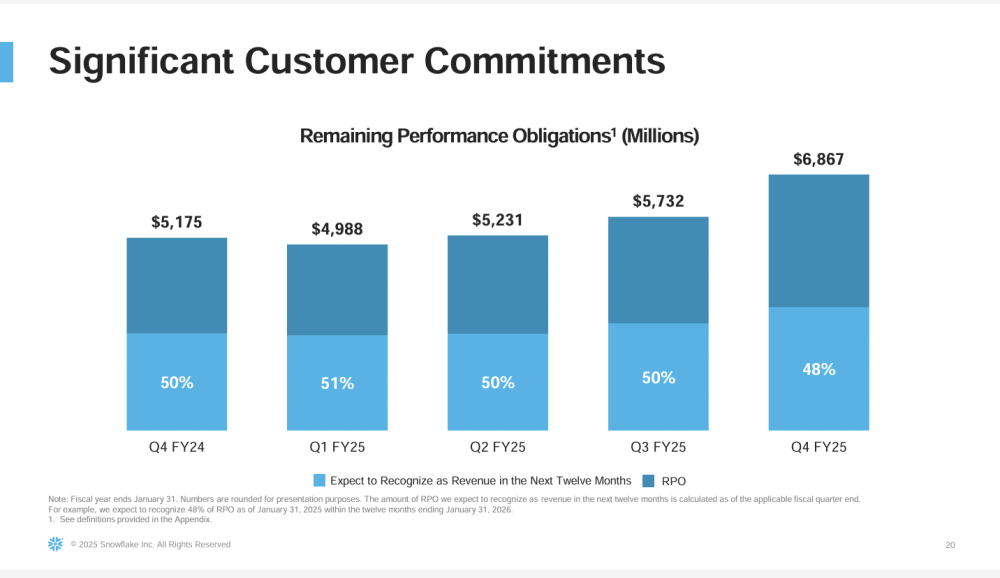

#7. RPO (Future Revenue) Growing Even Faster Than Current Revenue

A bullish sign for the future! Revenue isn’t just re-accelerating, but so are future bookings. That’s a bullish sign, especially paired with 126% NRR. The next few years look pretty bright!