PagerDuty was one of the more disruptive B2B apps when it lauched. We all used some sort of tool for website monitoring, but the O.G. PagerDuty just made it all so elegant, and so many of us quickly migrated to it. And when it IPO’d, it was still solidly an SMB solution.

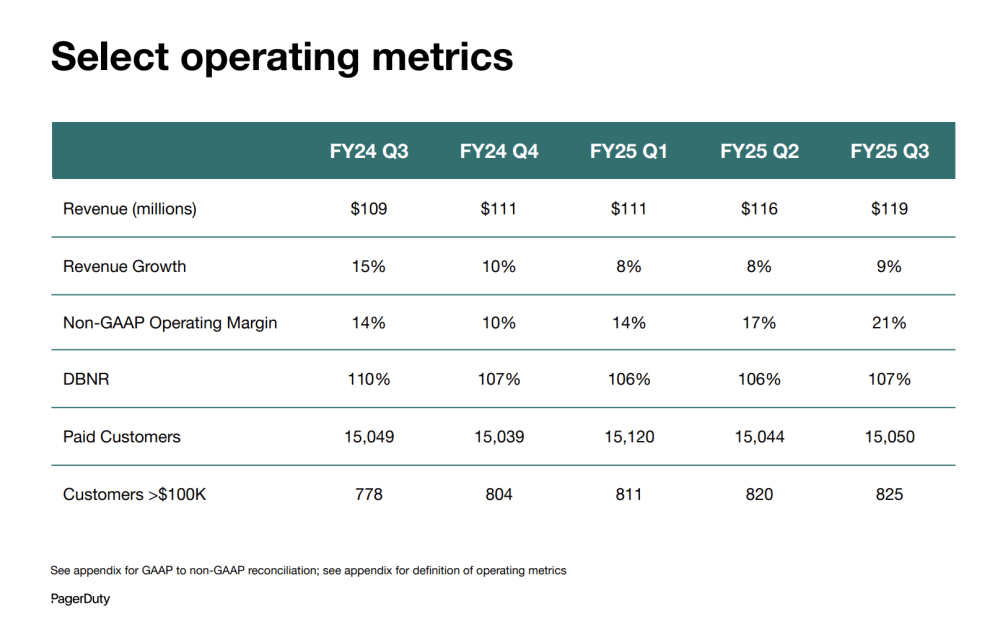

At IPO, at $125m ARR, PagerDuty had 10,000 customers and only 200 at $100k+ ACV.

Fast forward to today, and the world of DevOps has changed so, so much. As has PagerDuty. Today it’s a very enterprise solution, solving much bigger problems. And with a ton more competition:

$480,000,000 in ARR

Growing ARR 10%, slightly up

21% Non-GAAP Operating Margins

107% NRR and

0% net new customer growth. 15,050 today, vs. 15,049 a year ago.

Yields today:

$1.7B market cap, so about 3.5x ARR. This includes $540m of cash though, so net of cash, that’s closer to 2.5x ARR.

Today, PagerDuty today is a story of growth almost entirely fueled by strong NRR + its biggest customers. But they’ve doubled down on Free and the longest end of the tail, too, for future expansion.

5 Interesting Learnings:

#1. $100k+ Customers Up 6%

Overall customer count is flat, but PagerDuty is driving its 825 $100k+ customers up 6%.

#2. NRR at 107%, Although Down From 110% a Year Ago

This is the whole growth story at PagerDuty. 107% NRR fueling most of its 109% growth.

#3. Spending Less … Everywhere. So Operating Margins Are Way Up.

PagerDuty has leaned deep into getting efficient. Spending on sales & marketing is down. So is spending on product. And G&A.

#4. International Revenue is 28%

About in the middle for B2B.

#5. Growing Slightly Faster Than Before

Is it easy at PagerDuty today? No. But like many in B2B that saw a “downturn”, that downturn mostly ended in Q3’24 or so. PagerDuty isn’t predicting an easy year ahead. But it is predicting slightly higher growth than last year.

And a few other interesting learnings:

#6. Leaning More into Free

Even as it goes more enterprise, and see a decline in SMB / Commercial accounts, PagerDuty is still leaning in more on Free. It’s efficient. Paid customers are flat but total “customers” including Free are up 11%.

PagerDuty’s hand has gotten tougher. But they’ve stayed in the fight, doubling down on both $100k+ customers and Free customers. And getting very lean and efficient. And growth has reaccelerated — albeit to a small extent.

The public markets though aren’t in love with this much more efficient approach. A reminder it’s not all that simple.