5 Interesting Learnings from Freshworks at $800,000,000 in ARR

"Freshworks added 2,600 net customers last quarter, its largest net gain in four years."

So Freshworks started off as a low-end Zendesk competitor (Freshdesk), but relatively early expanded into a whole suite of related products for service and support, and most of its growth today is fueled by its lower-end competitor to ServiceNow, it’s “EX” products.

The support space has been turned upside down by AI, with as much as 40% of all support issues now handled by AI at many leaders. It’s one of the fastest-changing spaces in B2B.

And Freshworks has itself evolved. Today it’s at:

$800m ARR

Growing 22%

20% Free Cash Flow Margins

Modest re-acceleration in revenue growth and new customer count — but not NRR

Roots are SMB, but 60% of ARR comes from mid-market and enterprise today

And a $4B market cap, so 5x ARR

Freshworks is getting a bit of a second wind, which is great to see! Not an epic one, but a real one.

The 5x ARR multiple is a bit of a bummer, however,

5 Interesting Learnings:

#1. Modest Reacceleration Past Two Quarters

Sometime in Q3’24 might have been the end of the “downturn” in many B2B categories, per HubSpot and also here per Freshworks. You can see Freshworks is growing materially faster now than last year — 22% vs. 20%.

#2. Customer Count Also Modestly Re-Accelerating

Freshworks’ customer count was flat a year ago, but now is slowly growing again. Freshworks added 2,600 net customers last quarter, its largest net gain in four years.

#3. NDR/NRR Hasn’t Bounced Back, However

NRR is still flat / down. You really have to earn it in SaaS these days.

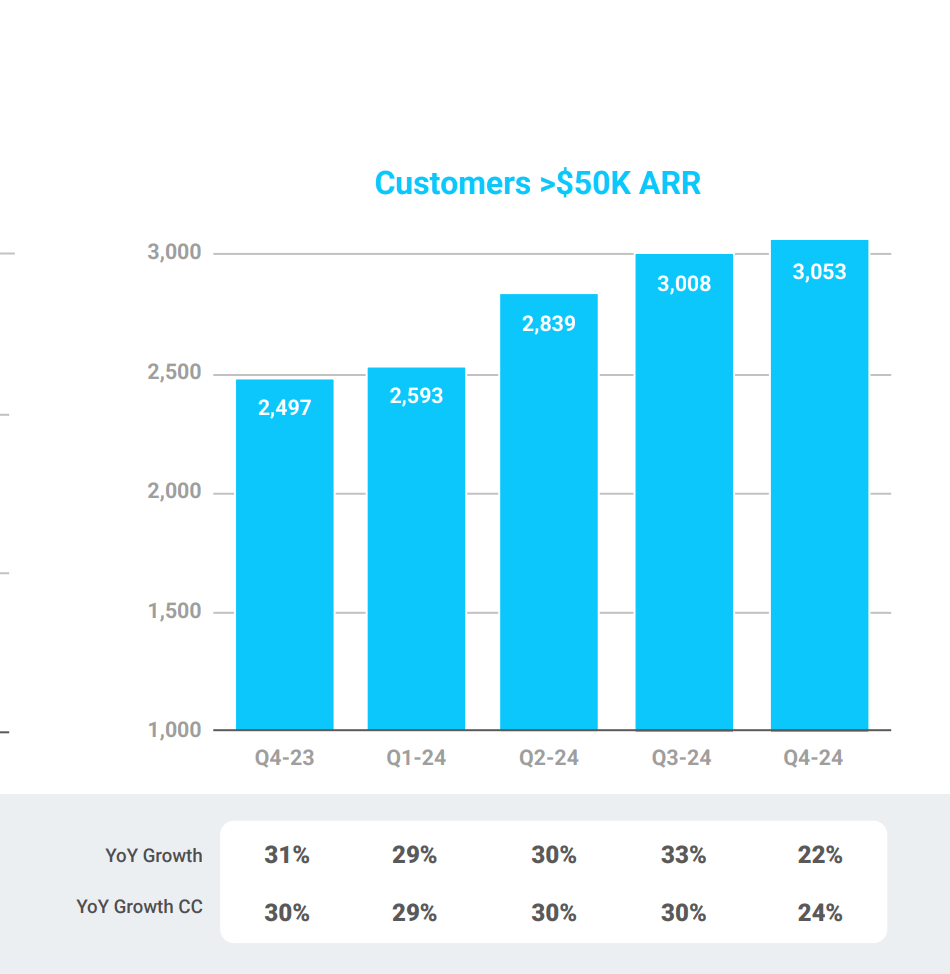

#4. Biggest Growth in $50k+ Customers, Who Are 50% of Revenue

The fact that NRR is flat even with $50k+ customers being the biggest driver of growth implies some contraction in smaller customers. In any event, like many from Zoom to Asana, the growth is mostly in bigger customers today. FBOW. 50% of revenue is now from $50k+ customers, and 90% from $5k+ customers.

#5. Its Roots May Be in India, But It’s as American and Global as Anyone in SaaS

Freshworks’ roots are in India, and it’s a hero company to many in SaaS in India. But the team has always been split between the U.S. and India, and the global revenue distribution is pretty similar to HubSpot’s overall. 47% of revenue in U.S., 53% in ROW:

And a few other interesting learnings:

#6. 50% Attach Rates for AI In $30k+ Deals, But Much Lower for SMBs

This is also what I’ve seen in the contact center. Deploying AI successful does require work, and the demand is higher in the enterprise.

#7. The Oldest Business, CX (Support) is Only Growng 7%. A Reminder How Important Going Multi-Product Is. Their EX Product is Primary Driver of Growth, Growing 33%.

If Freshworks had just stayed “Freshdesk”, it likely wouldn’t even be worth $1 Billion today.

#8. AI Leading to a 40%-50% Reduction in Average Ticket Handling Time, And Up to 40%-50% Deflection in Tickets Sent to Humans

This is what I am seeing overall in the space, and a realistic assessment of AI in support and CX. It can handle a lot of routine issues, quickly. Beyond that, many are handing off to a human today.

#9. A Cash Generating Engine Today, Expect to Generate $200m+ in Free Cash Flow This Year

Freshworks has gotten lean, but even as it has done so, it has modestly re-accelerated growth in both revenue and net new customers.

#10. Using Their Free Cash Flow Partially to Offset Dilution From Equity Grants. Less Than 1% Net Dilution After Repurchases.

When B2B companies burn cash and issue a lot of equity, the dilution can be fierce. But as you scale and get profitable, you can use your cash to buy back shares roughly equal to those you issue to new hires. That’s where Freshworks is today. Net dilution is less than 1%