5 Interesting Learnings from Datadog at $700,000,000+ ARR

More products = more revenue

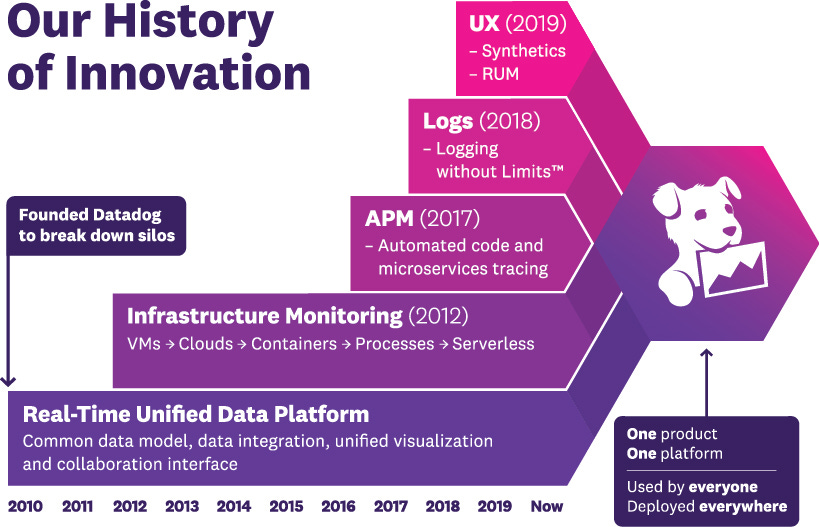

$30B+ Datadog became the great darling of developers and devops years ago, and never stopped pushing on the accelerator. It’s expanded its product portfolio with Logs, APM, and more to build an incredible observabillity engine approaching $1B ARR. At ~$700m ARR, Datadog was still growing an incredible 61% year-over-year.

Let’s take a look at 5 Interesting Learnings:

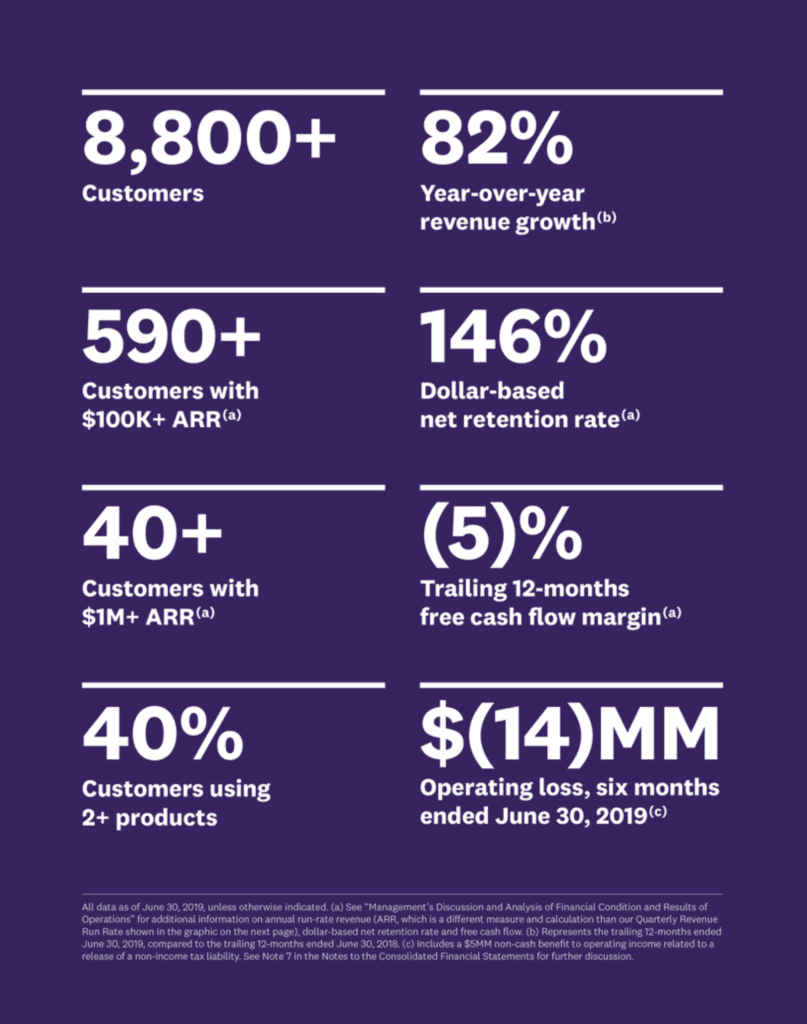

1. $100k+ customers generate 75% of revenue, even though just 7% of customers. Even with Free and Cheap editions to start, 75% of customers are or grow into $100k+ deals. Datadog has 1,107 $100k+ customers out of 13,100 total customers. That means the top 7% of customers generate 75% of revenue.

2. 20%+ of customers now use 4 or more products, and 70% use 2 or more products. This is a theme we’ve seen in this series. At Box, at Salesforce, and more, customers that use more products, buy more, pay more, and have higher NRR. 71% of customers are using two or more products, which is up from 50% last year. 20% of customers are using four or more products, which is up from only 7% a year ago. 75% of new logos landed with two or more products.

In addition, multiple products have enabled $100k customers to grow into $1m+ customers.

3. 60% of revenue growth comes from existing customers, and NRR > 130% for 13th consecutive quarter. This is similar to so many other Cloud leaders. At Salesforce, it’s 70%.

4. “Chunk up” payments from some annual deals. Some larger customers wanted semi-annual and monthly billing, and Datadog let them move there where it worked for them. Don’t over-push annual deals.

5. At IPO, Datadog already had 40+ $1M customers. From an acorn, a mighty oak can grow. Datadog shows customers can pay $1M+ at the same time as 10,000+ pay little and far more just use the Free version to get going. In fact, Datadog has several customers that have grown to $1M ARR in their first year using the products.

At IPO:

A few other notes:

6. Like most other SaaS and Cloud leaders, the Covid impact is over for Datadog. Retention, churn, usage growth, etc. are all, as a group, back to where they were before Covid hit.

7. Infrastructure is the entry point on product side, then 70% buy at least 1 more product. But Infrastructure is still where they come in.

8. Growing team as fast they can. They are hiring everyone great they can find in sales, engineering, and more. Hiring didn’t slow down at all even just as Covid hit.

9. Haven’t specialized salesforce yet. That’s interesting, given 4+ products and so many sizes of customers. Right now, it’s one salesforce selling all the products.

10. Limited pricing pressure, even with competitors offering more Free editions. Once you have a trusted brand, fair pricing can take you pretty far. Even when folks come in even cheaper.

11. Landing customers fast is more important than selling them more than 1 product. Even with 70% of customers now buying 2 or more products, Datadog focuses on getting a customer using 1 product quickly, and being happy.

12. Right now, partners generate very little revenue for Datadog. New partnerships with Microsoft, Google Cloud, and more are exciting. But right now, partners don’t directly generate material revenue for Datadog. Even now.

And a few other great ones in this series:

5 Interesting Learnings from Zendesk. As It Crosses $1B in ARR

5 Interesting Learnings from HubSpot as It Approaches $1 Billion in ARR

5 Interesting Learnings from RingCentral. As it Approaches $1B in ARR.

5 Interesting Learnings from Xero. As It Approaches $1B in ARR

5 Interesting Learnings from Snowflake at $600,000,000 in ARR

5 Interesting Learnings from New Relic at $650,000,000 in ARR