5 Interesting Learnings from Cloudflare at $1.7 Billion in ARR

"In the end, at scale, your largest customers are likely making up 50%+ of your revenue."

So Cloud and SaaS have had a bit of a rollercoaster the past 4 years, from the boom times of 2020-2021, to the tougher times overall of 2023, to the AI boom of 2024+. But one thing has done well through all of it: security. We always need it, and the threats keep coming.

And Cloudflare has been one of the biggest beneficiaries. It just keeps on going:

$1.7B+ ARR

28% growth (!)

15% non-GAAP operating profit, and 11% free-cash flow margins … and ..

a $39 Billion market cap (!!), up 45% in past 12 months (!!!)

Cloudflare is what 20x ARR looks like at scale, post-IPO. Top-tier growth, cash-flow positive, and very durable revenue. The last point is key. Wall Street wants revenue that is durable.

5 Interesting Learnings:

#1. 221,000 Total Paying Customers, But 65% of Revenue From 3,200 Large Customers

This is what you should see when a “long tail” engine is just working at scale. 100k+ paying customers, maybe even 1m+ free, but in the end, at scale your largest customers are likely making up 50%+ of your revenue. Just don’t neglect the small ones. They grow up into big ones!

#2. $400,000 in Revenue Per Employee

Cloudflare grew from $300k in revenue per employee at $1B ARR to $400k at $1.5B ARR or so and that seems to be its target to balance growth and efficiency.

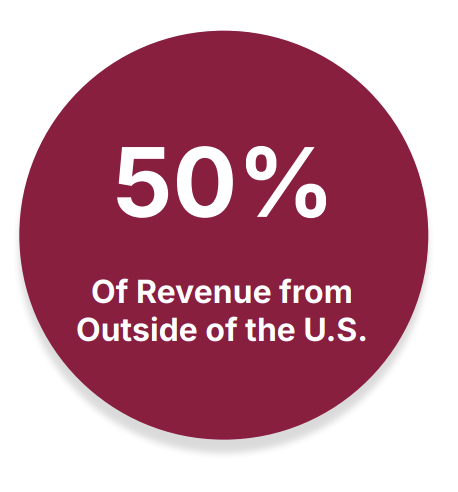

#3. 50% of Revenue Outside the U.S.

Our reminder to Go Global as early as you can.

#4. Self-Serve for Customers Of All Sizes — Not Just Small Ones

Cloudflare is committed to building a self-serve product that enterprises can try and buy on their own if they choose. It can be done! 🙂

#5. NRR Has Come Down a Bit, But Still Strong at 110%.

Clouldflare’s growth remains top tier, but it has come down a bit, and a dip in NRR is one of the reasons. 110% is still world-class. But it’s down from 115% a year ago. That makes growth 20%-30% harder than before.