5 Interesting Learnings from Atlassian at $4.4 Billion in ARR

"Atlassian isn’t immune from customers’ desires to cut and minimize seat count. It just hasn’t seen the dramatic impact there Salesforce and others have."

So we’ve covered Atlassian a lot on the 5 Interesting Learning series — for good reason. First, it’s a Cloud and SaaS leader we all look up to and know. And also, it’s interesting in that it straddles the line between business and developer markets. So while “B2B2B” has seen a lot of headwinds and challenges the past 24 months, the developer, infrastructure and Cloud side of the world has been stronger overall. Cloudflare, GitLab, etc. remain on fire.

So Atlassian as you’d expect is also in the middle. They not only grew 20% last quarter — but are still projecting 20%+ growth in the coming years — even at $4.4 Billion in ARR! (Although they are projecting a dip to 16% next year due to the wind down of migrating on-prem to Cloud customers). But they are also seeing some continued macro impacts at the same time.

5 Interesting Learnings:

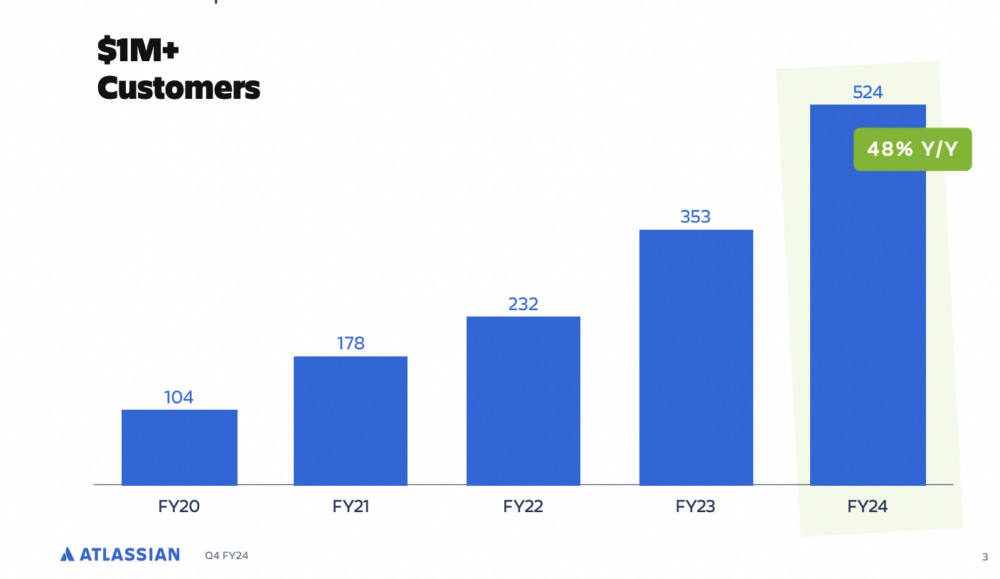

#1. $1m+ Customers Growing the Fastest (48%), With 98% Logo Retention

This isn’t unique to Atlassian, but a reminder of how much the biggest customers are the fuel for growth for many SaaS and Cloud leaders today. Not only are $1m+ customers growing 48%, but they stay. Logo retention is 98%+.

#2. $10k+ Customer Count Still Growing 18% a Year

It’s tough to stay in growth mode if your customer count doesn’t keep growing. Even at Atlassian’s scale, it’s still finding new customers. Its $10k+ customers are still growing 18% a year, and they now have 45,842 of them. Many SaaS and Cloud leaders are seeing new customer count slow or even stop. But not Atlassian. This is a very bullish sign for the next 5+ years. Note that overall, Atlassian has about 300,000 customers. So by customer count, the < $10k are still the vast majority. A reminder not to abandon the long tail, even as you pursue the bigger deals!

#3. Stunning Free Cash Margins of 37%

Almost 40% of every dollar Atlassian takes in goes to free cash flow. A pretty stunning cash engine at scale. They’ve generated $1.4 Billion in free cash from that $4.4 Billion in ARR. Software still rains cash — at least at scale!

#4. Managing Dilution to Less Than 2% a Year

Not a metric many worried about or called out at the peak of 2021 mania, but a key one today. Wall Street is extremely focused on the dilution costs of options and share-based equity, so managing this is a critical part of every pre-IPO and later SaaS and Cloud company today. It’s a tough one to get right.

#5. Planning to Hit $10B ARR in 5 Years

The beauty of recurring revenue and 100%+ NRR — that is, if you are also growing net new customer count too. Which is Atlassian is. You can predict long-term growth with fairly high confidence.

And a few other interesting learnings:

#6. Continuing to See Pressures on Seat Counts — And Plan to Continue to Increase Prices

Atlassian isn’t immune from customers’ desires to cut and minimize seat count. It just hasn’t seen the dramatic impact there Salesforce and others have. They also plan to offset this with more prices increases.

#7. 12,000 Employees, So About $370,000 in Revenue Per Employee

You don’t need to be here in the start-up phase. But the leaders in SaaS and Cloud all seem to be skating toward $400k in revenue per employee to hit Wall Street’s profitability expectations.

Did they disclose their NRR in latest earnings?