5 Interesting Learnings from Asana at $750,000,000 in ARR

"The SaaS downturn is over"

So the overall “project management” space has seen widely disparate impacts from the SaaS partial downturn of 2022-2024. Asana, strong in B2B2B and selling to tech, was perhaps hit hardest, with growth slowing to 10%. Monday.com by contrast, selling mainly outside of tech, saw growth remain strong at 34%. It’s been a tale of two worlds. SaaS that sells to B2B companies, and SaaS that sells to the Rest of the World. The former often had a tough time from 2022 to 2024. The latter? It was often close to the best of times.

AI though is the tailwind. It’s given Asana a boost, albeit it’s still early for AI at Asana. And the stock ralied, and while down a bit recently, is still up a stunning 52% over the past 6 months!

Today Asana is:

At $750,000,000 ARR

$4.75B market cap (so trading at 6x ARR or so)

Growing 10%

4% non-GAAP operating loss; not profitable or cash flow positive;

5 Interesting Learnings:

#1. NRR Fallen to 98% Overall, 99% For $100k+ Customers — From 115% at $600m ARR

This is half the reason growth has slowed at Asana. At $600m ARR, NRR has 115%. Today, it’s 98%-99%. While the root causes are multiple, from seat contractions in tech to budget scrutiny, at a higher level it’s a visceral remind of the importance of keeping NRR at 110%+. If Asana had the same NRR today it had even at $600m ARR, it would be growing twice as fast. And probably be worth 50% more.

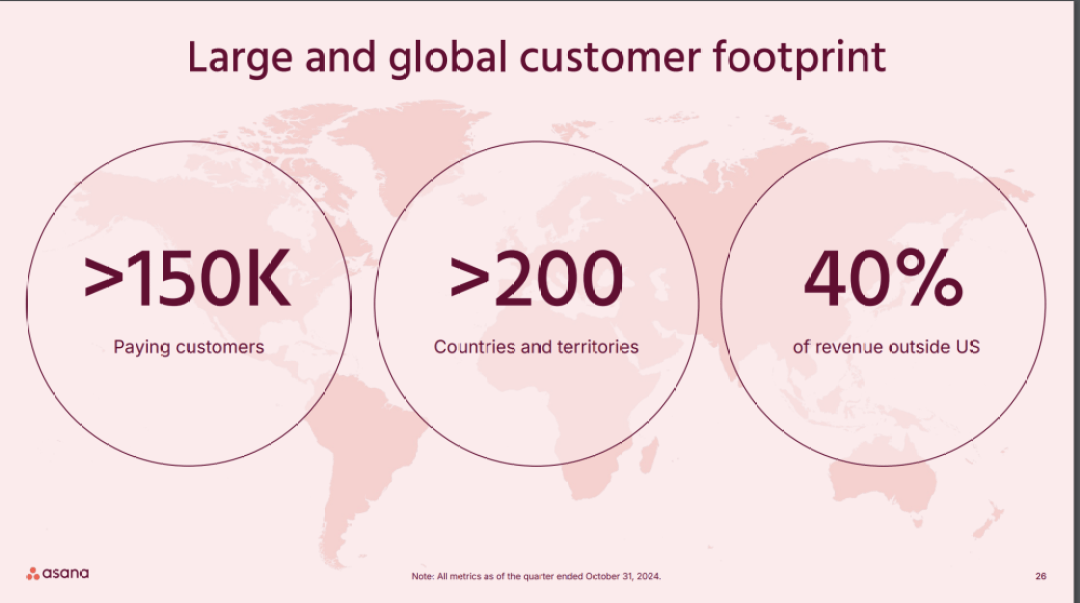

#2. 150,000 Total Customers. 100k+ Customers Are The Fastest Growing.

This isn’t unqiue to Asana, it’s true of many SaaS leaders at scale, from Zoom to Shopify. The enterprise customers are growing the fastest. Just remember not to leave the smaller ones behind!

#3. Getting More Efficient, But Not Profitable Yet

Asana has a PLG-SLG mix, but it’s a reminder PLG isn’t magically more efficient than SLG. Asana has gotten much more efficient, But it may not be non-GAAP “profitable” until $1B ARR.

#4. 40% of Revenue from Outside U.S.

Just our regular reminder to Go Global as early as you can.

#5. Pushing Into Non-Tech Verticals

Asana’s traditional strength has been in tech, but it has pushed outside of it to recapture growth. Non-tech verticals are growing 15%.

And a few other interesting learnings:

#6. Charging a Base Platform Fee for AI Studio, Then Variable Charge for Power Users

I think we’re all still figuring this out, but Asana will charge a platform fee for its AI studio and include a base amount of credits. And then charge users that go beyond 100s or 1000s of workflows per month. Will this stick? Is it too complicated, or is it what the market now expects? Let’s see!

#7. NRR Trending Slightly Back Up

There’s a general consensus that the B2B segments that saw a downturn the past 2 years saw that downturn end in Q3’24. That’s consistent with what Asana is seeing — a modest rebound in NRR:

AI Studio pricing model callout was interesting to see!